I've received a few calls about this and decided to write a short article. Scenario: My client recently finalized their divorce. As part of the settlement, client is required to pay monthly child support to their ex. During the process, my client incurred $6,000 in legal fees trying to negotiate and reduce the amount of child support they would have to pay. As tax season approaches, my client wonders if they can claim these legal fees as a tax deduction.

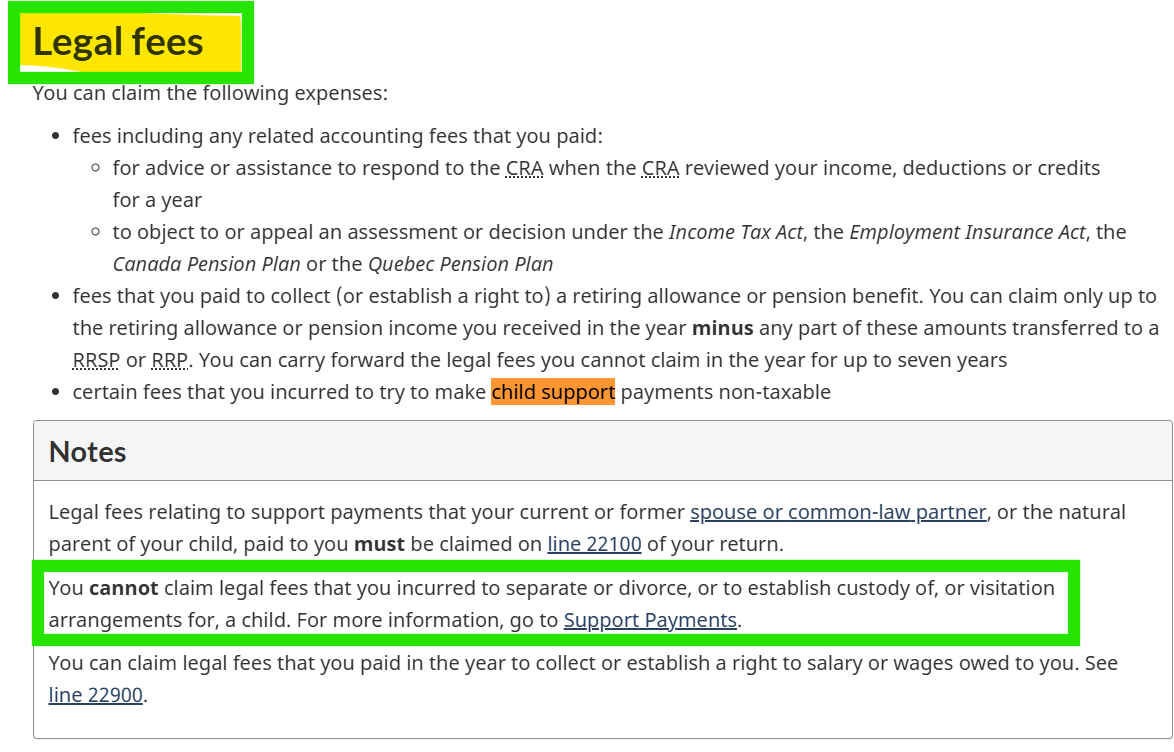

The short answer is: No. People who have to pay child support to their ex cannot deduct legal fees incurred to defend or dispute the child support. The Canada Revenue Agency does not allow child support payers to deduct legal fees incurred to negotiate, contest, reduce, or terminate child support payments. These expenses are considered personal or living expenses and are not deductible for tax purposes. This position is supported by court cases such as Grenon v. The Queen (2016 DTC 5009) and Landry v. The Queen (2014 DTC 1198).

Who Can Deduct Legal Fees? The recipient of child support may be able to deduct legal fees if they are incurred to establish, increase, or collect support payments. The payer, however, cannot deduct legal fees related to child support, regardless of the outcome.

If you are paying child support, legal fees related to those payments are not deductible. If you have questions about what expenses may be deductible during a divorce or separation, consult a tax professional for advice tailored to your situation.

Sources

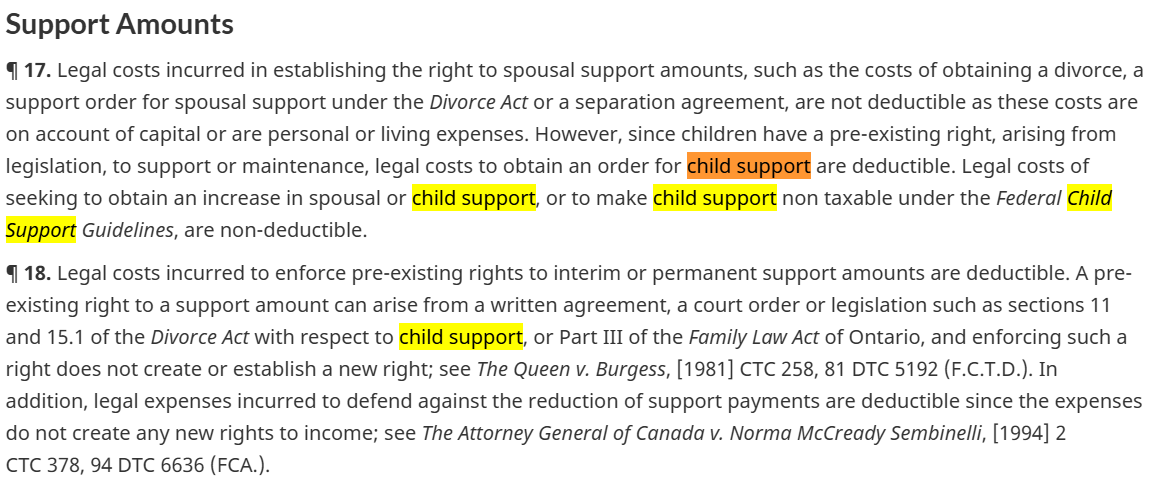

¶ 17. Legal costs incurred in establishing the right to spousal support amounts, such as the costs of obtaining a divorce, a support order for spousal support under the Divorce Act or a separation agreement, are not deductible as these costs are on account of capital or are personal or living expenses. However, since children have a pre-existing right, arising from legislation, to support or maintenance, legal costs to obtain an order for child support are deductible. Legal costs of seeking to obtain an increase in spousal or child support, or to make child support non taxable under the Federal Child Support Guidelines, are non-deductible.

¶ 18. Legal costs incurred to enforce pre-existing rights to interim or permanent support amounts are deductible. A pre-existing right to a support amount can arise from a written agreement, a court order or legislation such as sections 11 and 15.1 of the Divorce Act with respect to child support, or Part III of the Family Law Act of Ontario, and enforcing such a right does not create or establish a new right; see The Queen v. Burgess, [1981] CTC 258, 81 DTC 5192 (F.C.T.D.). In addition, legal expenses incurred to defend against the reduction of support payments are deductible since the expenses do not create any new rights to income; see The Attorney General of Canada v. Norma McCready Sembinelli, [1994] 2 CTC 378, 94 DTC 6636 (FCA.).

¶ 19. The legal costs described in ¶ 18 above are deductible even though an amount received as a "child support amount," as described in subsection 56.1(4), is not included in the income of the recipient. While "exempt income" in subsection 248(1) is defined as property received or acquired that is not included in income, the definition excludes "support amounts"; therefore, the deduction of costs incurred in respect of support amounts is not denied by virtue of paragraph 18(1)(c) as being exempt income. For a discussion of "support amount" and "child support amount," see the current version of IT-530, Support Payments.

¶ 20. A person who incurs legal expenses is not entitled to deduct them when they are incurred in connection with the receipt of a lump sum payment which cannot be identified as being a payment in respect of a number of periodic payments of support amounts that were in arrears. The lump sum payment however is generally not required to be included in income.

¶ 21. From the payer's standpoint, legal costs incurred in negotiating or contesting an application for support payments are not deductible since these costs are personal or living expenses. Similarly, legal costs incurred for the purpose of terminating or reducing the amount of support payments are not deductible since success in such an action does not produce income from a business or property. Legal expenses relating to obtaining custody of or visitation rights to children are also non-deductible.

--

If you need tax advice, speaking with a qualified CPA in Ottawa.

--

This is not legally binding tax advice. This is educational analysis. Say hello if you need help.

WhatsApp - 613.600.4194

--

Disclaimer

The information provided on this page is intended to provide general information. The information does not take into account your personal situation and is not intended to be used without a specific consultation. Lucas CPA Professional Corporation will not be held liable for any problems that arise from the usage of the information provided on this page.